European Tech-Enabled Business Services (TEBS): The Buy-and-Build Consolidation Map — 2026 Edition

An investment-grade consolidation map for mid-market PE — 15 sub-sector modules, cross-sector rankings, diligence toolkits, and platform thesis templates

European Tech-Enabled Business Services (TEBS): The Buy-and-Build Consolidation Map — 2026 Edition

Executive Summary (2026 Edition)

This report provides an investment-grade consolidation map for European Tech-Enabled Business Services (TEBS), tailored to mid-market private equity investors pursuing buy-and-build strategies. It is designed to be used in three moments of truth: (i) sector and geography screening, (ii) diligence and downside protection, and (iii) platform design (bolt-on sequencing, centralisation choices, and exit narrative construction). Across Europe, TEBS remains a dominant mid-market theme into 2026 as PE activity expectations rise in technology and business services and as buy-and-build continues to be the default execution model.

Chapter 1 — What TEBS is (and why it matters for multiples)

The report defines TEBS as service businesses where technology is a material driver of delivery efficiency, workflow embedding, data leverage, and/or revenue quality—without being pure SaaS. Two framing tools govern the entire analysis:

- Services-to-software continuum: TEBS value accretes as businesses move rightward—from labour-linear delivery toward workflow-embedded, recurring, low marginal cost models.

- Buy-and-build–ready sub-sector definition: attractive roll-up arenas combine fragmentation, standardisable operations, repeatable integration, resilient demand, and centralisation capacity.

A core underwriting distinction is made between:

- Multiple expansion through tech (tech changes unit economics and switching costs), versus

- Labour-driven scale (headcount + SG&A consolidation with limited re-rating potential).

Chapter 2 — Market structure and what separates 6× from 12× EBITDA

Using a disciplined “gross TAM vs TEBS-eligible TAM” construct, the report sizes European TEBS-eligible revenues at ~€350–450B (2025E) after adjusting for definitional eligibility and overlap. The key conclusion is that the investable TEBS perimeter is large enough to support many platforms, but narrow enough that definition discipline (what is truly tech-enabled) is a recurring source of alpha.

Three mandatory cross-sector exhibits drive screening:

- Services-to-software map: near-software positioning is most evident in Data & Analytics, Fund Administration, and workflow-embedded Insurance distribution; labour-heavy segments (e.g., Facilities, Staffing) sit leftward unless deliberately productised.

- Fragmentation × tech leverage matrix: the “sweet spot” combines high fragmentation with credible tech leverage (e.g., IT MSPs, Compliance, Data & Analytics, Insurance brokerage segments).

- 6× vs 12× driver framework: multiples are primarily shaped by recurrence, workflow switching costs, key-person dependency resolution, operational maturity, tech differentiation, and platform proof—with dispersion within sub-sectors often larger than between sub-sectors.

Chapters 3–5 — Sub-sector modules: where consolidation works (and why it fails)

Fifteen modules apply one consistent template (definition, size/fragmentation, target profile, buy-and-build attractiveness, tech levers, playbook, buyer landscape, failure modes). Key takeaways by cluster:

-

Top-tier “multiple-forming” roll-ups:

- IT Managed Services (MSPs): recurring revenue + automation + security attach create a repeatable integration and re-rating pathway—but tool-stack standardisation and talent scarcity are critical risks.

- Insurance Brokerage & Distribution: renewal-led recurrence, deep bolt-on density, and data-enabled cross-sell support the most consistent buy-and-build return profile; producer retention is the central diligence item.

- Compliance/Regulatory services: strong productisation potential; value creation hinges on converting projects to monitoring subscriptions and building workflow portals (avoid “portal as file dump” risk).

- Fund Administration / Financial back office: high switching costs and automation potential; integration risk concentrates in platform migrations and control environments.

- Data & Analytics services: highest tech ceiling, but also highest execution dispersion; winners institutionalise IP reuse, managed “run” contracts, and delivery standardisation.

-

Moat plays with slower tempo:

- TIC: accreditation provides defensibility and pricing power; integration must protect quality systems and capex discipline.

- Healthcare groups: extreme fragmentation and real procurement/scheduling synergies, but integration is fundamentally about clinical governance and clinician retention (not just systems).

-

Operational-alpha / density plays:

- Facilities management, staffing, engineering consulting, logistics control-tower models, environmental consulting, education/training can produce strong outcomes when underwritten as density + procurement + utilisation + contract repricing plays; tech is additive but rarely the primary multiple driver unless workflow embedding is demonstrably achieved.

-

Thesis-dependent / higher failure-rate roll-ups:

- Marketing/digital agencies (integration complexity + in-housing + AI content commoditisation) and Legal/LPO (AI substitution risk) require an explicit repositioning thesis toward managed services, outcomes pricing, and workflow embedding.

Chapter 6 — Consolidation map, rankings, and 2026–2028 white spaces

The report consolidates module scoring into a ranked map and groups sectors into four investable archetypes. The leading base-case sub-sectors are Insurance Brokerage and IT MSPs (both 4.3/5), followed by Compliance (4.0), Fund Admin (3.9), and Data & Analytics (3.8). The chapter also identifies white spaces by region (notably DACH and Southern Europe in selected verticals) and introduces the emerging AI services layer: TEBS firms increasingly act as the “AI distributor” for mid-market clients (implementation, governance, and managed operations), which strengthens the exit narrative when backed by usage and productivity evidence.

Chapter 7 — Buyer landscape and deal mechanics

Four buyer archetypes shape processes—software-native PE, services specialists, generalist mid-market funds, and strategics—each paying up for different attributes. Winning auctions in 2026+ requires (i) a credible 100-day integration plan presented early, (ii) clear centralise-vs-federate intent, and (iii) proof that “tech” moves unit economics (not AI theatre). The chapter provides IC-ready platform thesis templates (recurring tech-enabler, distribution compounder, density play, IP-led platform) and a practical exit readiness scorecard aligned to recurrence, integration proof, and tech defensibility.

Chapter 8 — Diligence toolkit, integration playbook, AI matrix, and outlook

The capstone provides deal-team-ready tools: a TEBS diligence checklist, a 100-day integration plan, an integration risk heatmap, and an AI impact matrix across all 15 sub-sectors. The AI conclusion is nuanced: most TEBS is structurally helped (augmentation), while Marketing/Agencies and parts of Legal/LPO face genuine substitution risk unless repositioned. The outlook emphasises consolidation acceleration in cyber-MSP, broker consolidation, alternatives operations platforms, and ESG/CSRD-related reporting ecosystems—tempered by persistent labour constraints in clinician- and engineer-heavy models.

Key Recommendations (IC-usable)

- Prioritise platform creation in five sub-sectors: Insurance brokerage, IT MSPs, compliance/regulatory services, fund administration, and data & analytics—where recurrence and workflow embedding most reliably convert into exit multiples.

- Underwrite “platform proof,” not just scale: require early evidence of KPI standardisation, tool-stack governance, and repeatable bolt-on integration cadence.

- Adopt the dominant integration model: centralise governance (finance, compliance, data, procurement, tooling rules) on Day 1; federate client relationships initially to protect retention.

- Treat AI as a value-capture mechanism, not a narrative: invest only where adoption and unit-economics uplift can be measured; avoid “AI theatre” via strict governance and before/after KPI proof.

- In labour-heavy sectors, underwrite operational alpha first: density, scheduling, procurement, and contract repricing should carry the base case; tech-enabled re-rating is upside, not the plan.

Chapter 1: Scope, Definitions, and Analytical Framework (How to Read and Use This Report)

1.1 Purpose and Intended Use

This report is a capital allocation and value-creation tool for mid-market private equity professionals evaluating buy-and-build opportunities across European Tech-Enabled Business Services (TEBS). It is designed to be used at three stages of the investment lifecycle: screening (which sub-sectors and geographies to prioritize), diligence (what to probe and what signals matter), and platform design (how to sequence bolt-ons, centralize operations, and construct an exit narrative).

The methodology in this chapter establishes the definitions, scoring rubrics, and analytical lenses that will be applied consistently across all 15 sub-sector modules (Chapters 3–5), the cross-sector synthesis (Chapter 6), buyer and deal mechanics analysis (Chapter 7), and the diligence and outlook toolkit (Chapter 8). Every claim in subsequent chapters is benchmarked against the frameworks defined here.

The market context is favorable. In the Roland Berger European PE Outlook, respondents expect Technology, software & digital solutions (69%) and Business services & logistics (68%) to see the highest number of PE M&A transactions in 2026. Deal commentary into 2026 also highlights an acceleration of mid-market buy-and-build strategies (smaller, complementary acquisitions to drive scale, synergies, and capability build). This report exists to help investment committees decide where within that broad thesis to deploy capital—and how to win.

Teaser (without premature ranking): Based on the framework defined in Sections 1.5–1.7, the report expects several sub-sectors to repeatedly screen well in the “Quadrant I” shape (high tech leverage, low integration complexity, high fragmentation)—often including IT managed services (MSPs), select TIC / compliance-led services, and workflow-embedded brokerage/administration models (examples only; final scoring is provided in Chapter 6).

Key assumptions (for how to interpret outputs)

| Assumption | Why it matters | Where it is used |

|---|---|---|

| Comparable multiple environment: H1-2025 mid-market multiple levels and dispersion are treated as the baseline reference for 2026 screening | Prevents false precision; keeps valuation discussion anchored to observable recent data | Chapters 2, 6–7; underwriting ranges |

| Tech enablement is measurable through unit-economics change (not “tooling presence”) | Avoids “tech-washing”; aligns screening with value creation reality | All sub-sector modules |

| Buy-and-build repeatability is a core determinant of attractiveness | Ensures sub-sector ranking reflects integration feasibility, not just market growth | Chapters 3–6 |

| Interview insights are directional, not statistical | Prevents overgeneralizing from expert samples | Sections 1.4–1.6; used for hypothesis shaping |

1.2 Core Definitions

1.2.1 Tech-Enabled Business Services (TEBS)

Definition: TEBS comprises services businesses where technology is a material driver of delivery efficiency, workflow embedding, data leverage, and/or revenue model quality—without the company being a pure software product company. The service is the core commercial offer; technology amplifies the margin, stickiness, and scalability of that service.

A company qualifies as “tech-enabled” when at least one of the following conditions is demonstrable:

- Delivery efficiency: Technology (workflow tools, automation, analytics) allows the company to deliver the same or better service output with materially fewer labor hours per unit of revenue than a non-tech-enabled peer.

- Workflow embedding: The company’s technology is integrated into the client’s daily operations (e.g., portals, monitoring dashboards, compliance platforms), creating switching costs that go beyond contractual lock-in.

- Data leverage: The company accumulates proprietary data through service delivery (benchmarking, risk scoring, performance analytics) that enhances its value proposition and can create network effects.

- Revenue model quality: Technology enables a shift from purely project-based billing toward recurring, subscription-like, or usage-based revenue streams with contractual visibility.

What TEBS is not: Pure SaaS companies selling licenses with no service component. Legacy labor-only services with cosmetic technology wrappers (e.g., a staffing firm with a basic ATS relabeled as “AI-powered”). Companies where technology is an internal support function but does not materially affect client-facing delivery or margin structure.

Why it matters for PE: As AI and automation increasingly shift support functions from “cost centres” toward “performance centres,” the investable surface area for tech-enabled services expands—but only where tech changes delivery economics and customer lock-in. TEBS businesses sit at the intersection of this transformation, offering the downside protection of contracted services revenue with the upside optionality of technology-driven margin expansion and multiple re-rating.

1.2.2 The Services-to-Software Continuum

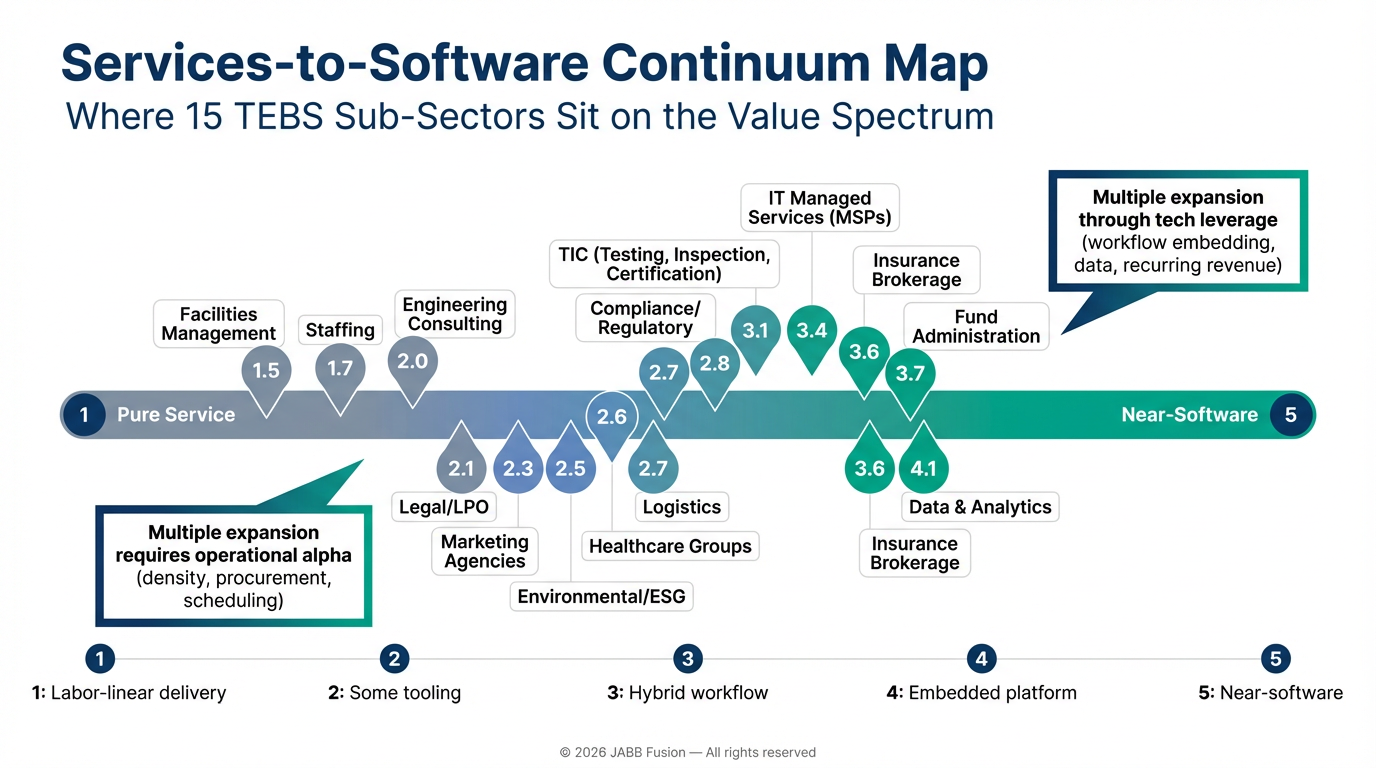

The services-to-software continuum is the spectrum along which business services companies are positioned, from pure labor delivery at one end to fully productized software at the other. Most TEBS targets occupy the middle ground, and their exact position has direct implications for entry multiple, margin trajectory, and exit narrative.

Positioning criteria (scored 1–5 for each target or sub-sector):

| Criterion | 1 (Pure Service) | 3 (Hybrid) | 5 (Near-Software) |

|---|---|---|---|

| Recurring revenue % | <20% | 40–60% | >80% |

| Software/workflow penetration | None; delivery is manual | Proprietary tools used internally to improve delivery | Client-facing platform; self-serve elements |

| Data/network effects | None | Some proprietary data informs service quality | Strong data moat; improves with scale |

| Delivery labor intensity | Revenue scales linearly with headcount | Partial automation; leverage on select functions | Minimal marginal labor per incremental unit of revenue |

| Client switching costs | Low; relationship-based only | Moderate; some integration/training required | High; embedded in workflow; data migration painful |

A sub-sector’s position on this continuum is not static. A central TEBS private equity thesis is to move a portfolio company rightward on the continuum during the hold period—increasing recurring revenue, deepening workflow embedding, and building data assets—thereby justifying a higher exit multiple.

1.2.3 Buy-and-Build–Ready Sub-Sector

Definition: A sub-sector is “buy-and-build–ready” when the following minimum conditions are met:

- Fragmentation: The top 5 players hold less than 25% market share in the target geography, with a dense long tail of acquisition candidates at €1–15M revenue.

- Standardizable operations: Core service delivery can be codified into repeatable processes, allowing centralized training, quality control, and back-office consolidation.

- Repeatable integration: Bolt-on acquisitions follow a predictable playbook (e.g., financial integration within 60 days, systems migration within 6 months, commercial harmonization within 12 months).

- Ability to centralize/enforce playbook: A platform can extract value through shared services (finance, HR, procurement, IT), centralized pricing, and standardized reporting without destroying local client relationships.

- Resilient demand: The underlying service addresses a non-discretionary or structurally growing client need (e.g., compliance, IT infrastructure, healthcare, building maintenance) with low cyclicality relative to GDP.

With elevated entry multiples for platform investments, sponsors have leaned further into buy-and-build strategies (particularly in the mid-market), using add-ons as a core mechanism to compound value creation.

1.2.4 Standalone definition: “Multiple Expansion Through Tech” vs. “Labor-Driven Scale”

These are two distinct value-creation models that can look superficially similar in an investment memo (“we will professionalize, consolidate, and grow”) but underwrite to different outcomes.

Multiple expansion through tech (definition): A value-creation model where technology meaningfully improves delivery unit economics and customer switching costs, shifting the business rightward on the services-to-software continuum—and enabling a credible exit as a “technology-powered platform,” not merely a larger services consolidator.

Labor-driven scale (definition): A value-creation model where growth and EBITDA expansion primarily come from adding people, expanding footprint, and consolidating SG&A—without a step-change in delivery unit economics or workflow embedding. The exit narrative is predominantly “scaled services group.”

1.2.5 Diagnostic indicators (how to tell which model you are underwriting)

Multiple Expansion Through Tech — Diagnostic Indicators:

- Gross margins expand by ≥300 bps within ~24 months of technology investment (automation, workflow tools, analytics).

- Revenue per employee grows faster than headcount.

- Recurring or contract-based revenue share increases (e.g., from ~35% to 55%+).

- Client-facing technology creates switching costs observable in retention metrics (e.g., net revenue retention ≥95% where NRR is applicable).

- At exit, the business can credibly be positioned as a “technology-powered platform,” which is where higher valuation ranges are more frequently observed in market evidence.

Labor-Driven Scale — Diagnostic Indicators:

- Revenue growth requires near-proportional headcount growth.

- Gross margins remain broadly stable (no operating leverage from technology).

- Key-person dependency persists at the delivery level.

- Bolt-ons primarily add revenue and geographic coverage, but do not change delivery unit economics.

- Exit multiple remains in the services band (typically lower than tech-enabled outcomes), consistent with observed services-heavy valuation ranges.

Valuation linkage (evidence anchor): European mid-market M&A multiples in 2025 vary materially by sector and quality; market monitors show a broad band in which technology-adjacent assets typically clear higher ranges than traditional services. This report’s screening question is therefore explicit: Does technology change the unit economics of delivery and switching costs—or does it merely support the back office?

1.3 Geographic Scope and Segmentation

Covered Regions

This report covers six European country clusters:

| Cluster | Countries | Rationale |

|---|---|---|

| UK & Ireland | UK, Ireland | Largest single-country PE market in Europe; English-language; high services GDP share |

| Nordics | Sweden, Norway, Denmark, Finland | High digital maturity; dense PE activity; buy-and-build culture |

| DACH | Germany, Austria, Switzerland | Mittelstand fragmentation; largest continental economy; strong industrial services base |

| Benelux | Netherlands, Belgium, Luxembourg | Open economies; headquarters density; cross-border operating norms |

| France | France | Large market; distinct dynamics; recent political uncertainty affecting deal flow |

| Southern Europe | Spain, Italy, Portugal, Greece | Growing PE activity; lower multiples; fragmentation opportunity |

Roland Berger’s outlook indicates Central and Eastern Europe (CEE) is expected to see one of the strongest gains in momentum by region (with DACH and Nordics also highlighted). While CEE is not a primary focus region in this report, it is referenced as a nearshoring and expansion destination where relevant to TEBS platform strategies.

Comparability Approach

- Currency: All financials are expressed in euros (€). UK figures are converted using the prevailing GBP/EUR rate as of Q4 2025 (approximately £1 = €1.14, directional). Swiss franc figures are converted at CHF/EUR ~0.95 (directional, period-typical). Nordics are converted at prevailing SEK, NOK, and DKK rates.

- Normalization: EBITDA margins, multiples, and growth rates are reported on a pre-IFRS 16 basis where possible to maintain comparability with private company financials. Where only post-IFRS 16 data is available, the adjustment is noted.

- Size segmentation: “Mid-market” in this report refers to enterprise values of €20M–€500M for platform investments and €2M–€50M for bolt-on acquisitions. Revenue ranges for targets are stated at the sub-sector level.

1.4 Sources, Evidence Standards, and Limitations

Data Stack

This report triangulates findings from multiple source layers:

- Deal databases / market monitors: Deal volumes and mid-market valuation observations are triangulated across databases and mid-market publications (PitchBook, Mergermarket, Unquote, S&P Capital IQ) and mid-market monitors such as Dealsuite. Dealsuite reports an H1-2025 average European EBITDA multiple of ~5.3×, with dispersion by region (e.g., DACH, France, Netherlands as reported).

- Public company comps: Listed European comparables are used as benchmarks for margin structure, growth, and valuation logic (e.g., Adecco, Bureau Veritas, Capita, Homeserve, Halma).

- Broker and advisor reports: M&A advisor intelligence is used for observed activity levels and sector mix. RSM reports advising on 768 completed deals in 2025, with sector breakdown including engineering & manufacturing (156), business services (152), and TMT (146).

- Industry benchmarks: Sector reports from IBISWorld, Eurostat, national statistics offices, and trade associations are used for market sizing, fragmentation analysis, and labor market context.

- Interview program (target personas): Analytical conclusions are informed by structured interviews with PE operating partners (N=25+), TEBS platform CEOs (N=15+), M&A advisors specializing in business services (N=10+), and technology consultants supporting PE portfolio companies (N=10+). Interviews are used to generate and stress-test hypotheses; they are not treated as statistical evidence.

- Web-scraped proxies: Job posting density (Indeed, LinkedIn) as a proxy for labor market tightness and company growth trajectories; pricing pages and service descriptions as proxies for technology maturity; review sites (e.g., Trustpilot, G2) for quality benchmarking.

- Triangulation logic: No single data point is taken at face value. Market sizes are expressed as ranges with stated methodology. Multiples are benchmarked against at least two independent sources where possible. Qualitative claims are tested against multiple evidence types (deal evidence, public-company analogies, and/or expert input).

Evidence standards (what “good” looks like in this report)

- Quantified claim = cited claim: Any percentage, multiple, deal count, or region-by-region numeric statement is accompanied by an inline citation (e.g.,,,).

- Directional claim = anchored claim: Macro or thematic statements (e.g., “buy-and-build is gaining traction”) are anchored to reputable commentary and/or market monitors.

- No false precision: When sources provide ranges or averages, the report uses ranges/approximations (e.g., “~5.3×”) rather than implying exactness.

Limitations and explicit assumptions (expanded)

- Multiple persistence assumption (2025 → 2026): Where the report references 2025 mid-market multiple levels and dispersion (e.g., Dealsuite H1-2025), it uses them as a baseline reference frame for 2026 screening rather than a forecast. The implicit assumption is that relative dispersion by sector quality (tech-enabled vs labor-driven) remains directionally informative into 2026, even if absolute levels move with rates and risk appetite.

- Database coverage bias: Mid-market deal databases and monitors can under-represent smaller proprietary transactions and may reflect reporting bias by geography and advisor ecosystem density. Conclusions are therefore triangulated with advisor reports and interviews.

- Interview representativeness: The interview sample is intentionally skewed toward active PE value-creation and M&A practitioners; it is not representative of the full universe of TEBS operators. Interview insights are treated as hypothesis-generating and are validated against market evidence where feasible.

- FX comparability: GBP/EUR and other conversion rates are used for readability and comparison, not for hedging, treasury, or forecasting. The report uses a Q4-2025 directional GBP/EUR reference (~1.14) and does not model FX sensitivity unless material to a case.

- Accounting normalization: Private company EBITDA definitions vary (owner add-backs, capitalization policies, IFRS 16 treatment). The report flags comparability issues where known and avoids over-weighting single-point EBITDA margin comparisons.

- Regulatory and labor nuance: The report does not perform jurisdiction-by-jurisdiction legal analyses; regulatory references are included only when they materially affect fragmentation, switching costs, pricing power, labor supply, or integration feasibility (i.e., core underwriting variables).

What This Report Will NOT Do

- No compliance-heavy regulatory deep dives. Regulation is mentioned only where it directly and materially affects fragmentation, scalability, labor availability, pricing power, or barriers to entry.

- No false precision on market sizing. TAM figures are directional ranges with stated assumptions, not spuriously precise numbers.

- No AI hype. AI is assessed as a strategic lever with specific EBITDA-impact pathways; claims are subjected to evidence tests. Chapter 8 includes an AI impact matrix distinguishing structural help, structural threat, and neutrality by sub-sector.

1.5 Core Analytical Framework

The following four-pillar framework is applied to every sub-sector analysis in Chapters 3–5 and informs the cross-sector synthesis in Chapter 6.

1.5.1 Fragmentation and Bolt-On Density

How measured:

- CR5 (Concentration Ratio of top 5 firms) in the relevant geography: <25% = highly fragmented; 25–50% = moderately fragmented; >50% = concentrated.

- Bolt-on density: Estimated number of acquisition candidates at €1–15M revenue within the target geography, normalized per €1B of addressable market. A density of >30 candidates per €1B TAM is rated “high.”

- Founder/owner-operator share: Percentage of target-sized businesses that are founder-owned, family-owned, or nearing generational transition. Higher share = greater pipeline of motivated sellers.

What “good” looks like: CR5 <20%, bolt-on density >40 per €1B TAM, >60% founder-owned in the target size range. These conditions create a structurally favorable environment for buy-and-build.

1.5.2 Margin Expansion Levers Taxonomy

Every TEBS sub-sector has a specific set of margin expansion levers. We categorize them into eight types and assess applicability for each sub-sector on a 1–5 scale:

| Lever | Description | Where It Works Best |

|---|---|---|

| Pricing | Shifting from hourly/project billing to value-based, subscription, or retainer pricing | Advisory, TIC, compliance services |

| Utilization | Increasing billable hours as a % of total hours through better scheduling, demand forecasting, and bench management | Staffing, consulting, engineering |

| Procurement | Centralizing purchasing of materials, subcontractors, licenses, and tools across the platform | Facilities management, IT MSP, dental/vet |

| Delivery automation | Replacing manual process steps with software, RPA, or AI-assisted workflows | Back-office services, legal process, data analytics |

| Near/offshoring | Moving lower-value-add delivery steps to lower-cost geographies | IT services, marketing, legal process |

| Shared services | Centralizing finance, HR, IT, and compliance functions across the platform | All sub-sectors (universal lever) |

| Vendor consolidation | Reducing tool and vendor sprawl across acquired entities | IT MSP, marketing services, facilities |

| SKU rationalization | Simplifying and standardizing the service offering portfolio | Marketing agencies, engineering consulting |

1.5.3 Scalability Without Proportional Labor Growth

This pillar measures whether a business can grow revenue without a linear increase in headcount—the defining characteristic that separates tech-enabled services from traditional services.

Signals (scored 1–5):

- Automation rate: Percentage of delivery steps that are fully or partially automated. >30% = strong.

- Span of control: Average number of direct reports per manager. Improving span of control without quality degradation indicates operational leverage.

- Tooling adoption: Percentage of delivery staff actively using proprietary or standardized workflow tools. >80% = strong.

- Workflow standardization: Degree to which service delivery follows documented, repeatable processes (vs. bespoke, consultant-dependent approaches).

- Revenue per FTE growth: Target of >5% annual growth in revenue per FTE (inflation-adjusted) as a baseline indicator of operational leverage.

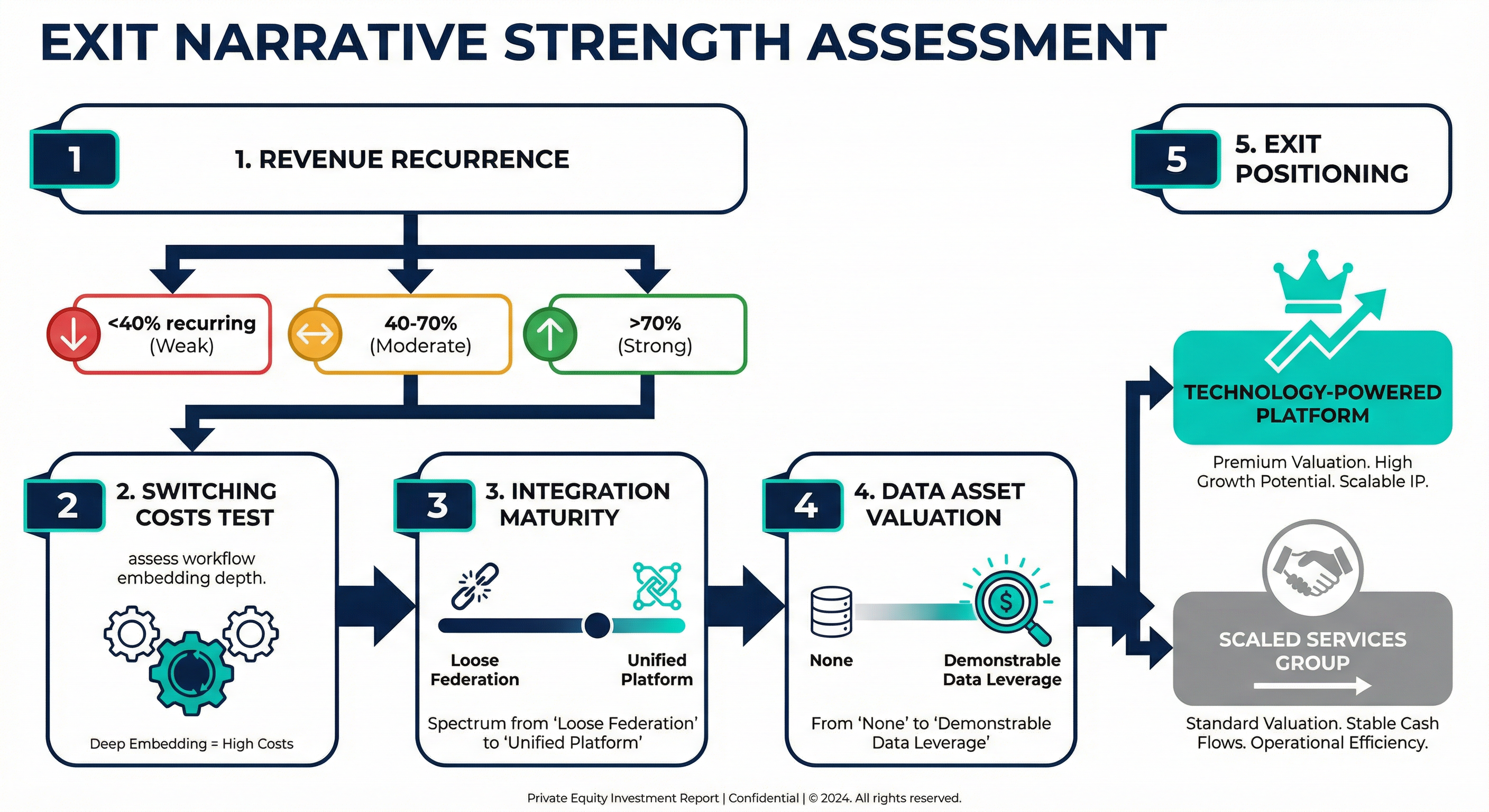

1.5.4 Exit Narrative Strength

Buyers pay premium multiples for durability and downside protection in uncertain macro conditions. The more an acquirer pays at entry, the greater its need to deliver material operational value creation; at exit, the story must resonate with the next buyer’s underwriting criteria.

What buyers reward in 2026+ (each scored 1–5):

- Recurrence: >70% of revenue is recurring or contracted.

- Defensibility: Switching costs, regulatory moats, proprietary data, or embedded workflows reduce churn structurally (e.g., <5% gross revenue churn annually where meaningful).

- Data assets: Proprietary datasets that improve with scale and are demonstrably used in delivery or client-facing analytics.

- Integration maturity: Unified tech stack, shared KPI dashboard, standardized commercial processes.

- Platform density: ≥5 bolt-ons with demonstrable synergy realization and repeatable integration capability.

1.6 Deliverable Templates and Scoring Rubric

1.6.1 Sub-Sector Module Template (Headings A–H)

Every sub-sector module in Chapters 3–5 follows this identical structure:

| Section | Content | Purpose |

|---|---|---|

| A. Definition & Scope | What’s in/out; where “tech-enabled” shows up in practice | Boundary-setting for screening |

| B. Market Size, Growth, Fragmentation | TAM (range), CAGR, CR5, bolt-on density, cross-border variation | Investment opportunity sizing |

| C. Typical Target Profile | Revenue range, margin profile, ownership type, geographic footprint | Target identification |

| D. Buy-and-Build Attractiveness | Fragmentation, bolt-on density, integration complexity, standardization potential | Thesis viability assessment |

| E. Technology Levers | Core systems, automation, data/AI; tie to EBITDA and scalability | Value creation scoping |

| F. Value Creation Playbook | Centralization, pricing, cross-sell/upsell; sequencing (0–12, 12–36 months) | Post-close planning |

| G. Buyer Landscape | Active PE archetypes, strategics, entry/exit dynamics | Competitive positioning |

| H. Red Flags & Failure Modes | Integration mistakes, margin illusions, key-person risk, churn triggers | Risk mitigation |

Each module also includes a mandatory per-sub-sector table with four fields:

- Target Signal Checklist: 8–12 observable screening signals.

- Core KPIs: 6–10 diligence and operating metrics.

- Margin Expansion Levers: Applicable levers (Section 1.5.2) with estimated EBITDA impact ranges (bps), explicitly labeled as estimates.

- Technology Maturity Benchmarks: Best-in-class vs lagging stacks with adoption indicators.

1.6.2 Buy-and-Build Attractiveness Scoring Model

Each sub-sector is scored on six dimensions using a 1–5 scale (5 = most attractive). The composite score is a weighted average.

| Dimension | Weight | 1 (Least Attractive) | 3 (Moderate) | 5 (Most Attractive) |

|---|---|---|---|---|

| Fragmentation | 20% | CR5 >50%; few targets | CR5 25–50% | CR5 <20%; dense long tail |

| Integration Complexity | 20% | High; bespoke delivery; cultural fragility | Moderate; some standardization possible | Low; repeatable integration playbook |

| Tech Leverage | 20% | Minimal tech impact on margins | Some automation/tools; incremental benefit | Technology transforms unit economics |

| Pricing Power | 15% | Commodity service; aggressive procurement | Some differentiation; moderate stickiness | Mission-critical; high switching costs |

| Labor Risk | 10% | Severe shortages; wage inflation; key-person dependency | Manageable with effort | Low dependency; automated delivery; broad talent pool |

| Exitability | 15% | Narrow buyer universe; services multiples only | Multiple exit paths | Strong narrative; tech premium plausible |

Composite score interpretation:

- 4.0–5.0: Priority sub-sector for immediate platform thesis development

- 3.0–3.9: Attractive with caveats; thesis-dependent

- 2.0–2.9: Selective opportunities only; requires specific angle

- <2.0: Avoid or wait for structural change

1.6.3 Target Signal Checklist Structure

Target signals are observable indicators—detectable through desk research, broker conversations, or early-stage diligence—that a company is a strong candidate for a TEBS buy-and-build acquisition. Each signal links to a specific diligence question.

| Signal Category | Observable Indicator | Diligence Question |

|---|---|---|

| Revenue Quality | >50% recurring/contracted revenue; multi-year agreements | What % of revenue is contractually committed beyond 12 months? What are gross and net revenue retention? |

| Growth Trajectory | Organic revenue growth >8% CAGR over 3 years | What is the split between volume, pricing, and new customers? Any dependency on a single vertical? |

| Margin Profile | EBITDA margin >12% (services) or >18% (tech-enabled) | What is margin by service line? Where is expansion post-centralization? |

| Owner Dynamics | Founder aged 55+; no succession plan; or sponsor nearing exit | What is the seller’s motivation? Is there a bench below the founder? |

| Technology Posture | Proprietary tools/portals/data assets; R&D spend >3% revenue | Is tech client-facing or purely internal? What switching costs exist? |

| Customer Base | Top 10 clients <40% of revenue | What is CAC and payback? Contract duration and renewal dynamics? |

| Scalability | Revenue per FTE growing >5% p.a.; standardized workflows | How many standard delivery processes exist? Onboarding time? |

| Bolt-on Potential | Clear adjacency map in niche/geography | How many similar businesses exist and are approachable? |

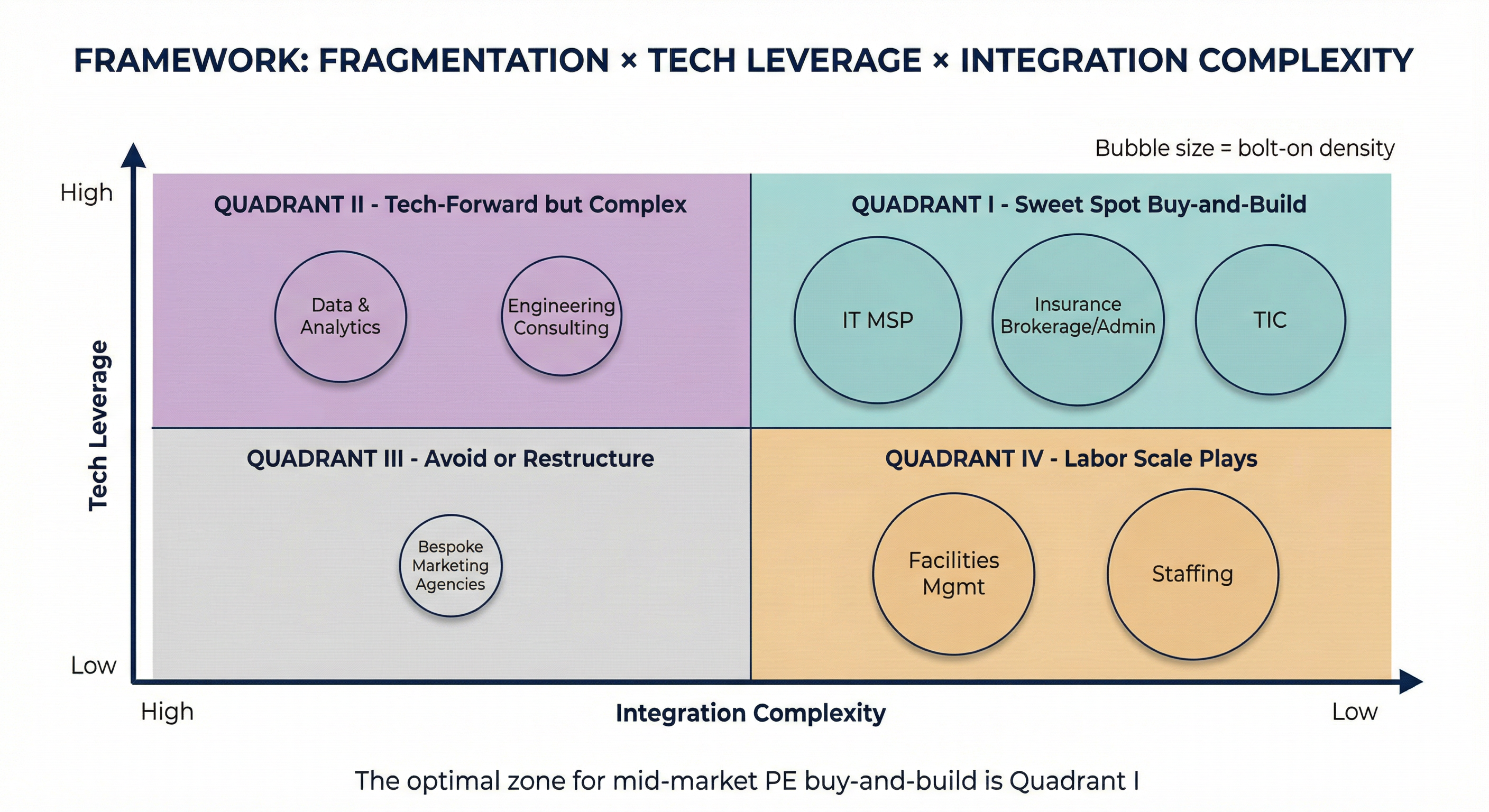

1.7 Framework Diagram: Fragmentation × Tech Leverage × Integration Complexity

The third dimension—fragmentation (represented by bubble size in a scatter plot)—determines bolt-on density. The optimal zone for mid-market PE buy-and-build is Quadrant I (high tech leverage, low integration complexity, high fragmentation). Quadrant IV can also work for sponsors with strong operational playbooks willing to accept services-level multiples. Quadrant II requires specialist investors with deep sector expertise and tolerance for integration risk. Quadrant III is generally avoided unless there is a credible thesis to shift the segment rightward on the tech continuum (Section 1.2.2).

1.8 Scope Exclusions and Boundary Conditions

To maintain analytical focus, the following are explicitly out of scope:

- Pure software/SaaS companies with no services delivery component.

- Large-cap transactions (EV >€500M at entry) except as exit comparables.

- Non-European geographies except for US comparisons that illuminate European dynamics.

- Regulatory deep-dives beyond what is required to understand fragmentation, pricing power, switching costs, and scalability.

- Macro forecasting: The report does not predict interest rates, GDP growth, or exchange rates. Where macro assumptions affect conclusions, they are stated explicitly and sensitivity-tested qualitatively.

1.9 How to Use This Report

For PE Partners and IC Members:

- Start with Chapter 2 (market landscape and valuation drivers) to calibrate where TEBS sits in your sector allocation.

- Use the scoring rubric in this chapter and the consolidated view in Chapter 6 to prioritize sub-sectors.

- Reference specific sub-sector modules (Chapters 3–5) when evaluating live deal opportunities.

For Investment Managers:

- Use the Target Signal Checklists to accelerate screening.

- Reference the Margin Expansion Levers Taxonomy to build underwriting cases.

- Use the buyer landscape analysis in Chapter 7 to position competitively in auctions.

For Operating Partners:

- The Value Creation Playbooks in each sub-sector module provide sequenced 0–36 month action plans.

- The Integration Playbook in Chapter 8 provides cross-cutting 100-day priorities.

- The AI Impact Matrix in Chapter 8 distinguishes structural help vs threat, grounded in operational pathways rather than “AI narratives”.

For M&A and Value-Creation Teams:

- The Diligence Checklist in Chapter 8 is designed for direct use in live deal workstreams.

- The Platform Thesis Templates in Chapter 7 provide IC-ready frameworks for new platform proposals.

- The cross-border expansion playbooks address the commercial and cultural considerations of scaling TEBS platforms across European borders.

Given the continued emphasis on buy-and-build, the quality of post-merger integration is increasingly the determinant of outcome dispersion. In parallel, private market commentary stresses a tougher operating environment that increases the premium on demonstrable operational value creation (not financial engineering). This report provides the frameworks and evidence base to do both systematically.

Chapter 2: The European TEBS Landscape: Market Structure, Value Accrual, and What Drives 6× vs 12× EBITDA

2.1 Market Structure Overview: Aggregate TEBS TAM and Sub-Sector Decomposition

2.1.1 Sizing the European TEBS Opportunity (and Reconciling “Sector TAM” vs “TEBS-Eligible TAM”)

The European Tech-Enabled Business Services (TEBS) market does not map neatly to a single classification system. As defined in Chapter 1 (Section 1.2.1), TEBS is a cross-cutting investable perimeter spanning fifteen service sub-sectors, but only the portions where technology is (i) material to delivery economics and/or (ii) credibly investable as a workflow-embedded value-creation lever.

This distinction resolves the major sizing pitfall in many TEBS discussions:

- “Sector TAM” (gross market) = total revenues in the broad service category (e.g., total staffing, total facilities management).

- “TEBS-eligible TAM” (this report’s TAM) = the subset of revenues where tech enablement is a meaningful driver of repeatable unit economics, scalability, and multiple formation (e.g., RPO/MSP/VMS-enabled staffing; CAFM/IoT-enabled FM; managed outcomes vs ad hoc projects).

Key correction (consistency fix): In the prior draft, the stated aggregate TEBS TAM (€350–450B) was inconsistent with the sum of the gross sector TAMs shown in Table 2.1.2 (>€600B low-end). In this refined chapter, Table 2.1.2 explicitly separates gross sector TAM from TEBS-eligible TAM and shows the eligibility factor used to bridge the two. The aggregate TEBS TAM is now mechanically reconcilable to the table.

Bottom-up aggregate estimate (2025E)

- Sum of TEBS-eligible TAM across the 15 sub-sectors: ~€320–475B (ranges reflect both market uncertainty and eligibility-factor uncertainty).

- Less overlap adjustment: Several revenue pools can be double-counted across sub-sectors (e.g., “data & analytics services” embedded in IT services contracts; compliance work embedded in legal and advisory mandates). We apply a conservative ~5–10% overlap haircut to avoid overstating addressability.

- Resulting aggregate European TEBS-eligible TAM (2025E): €350–450B.

This aggregate range is directionally validated by public market proxies used as triangulation inputs (all converted consistently to EUR using an illustrative USD/EUR = 0.92 FX assumption for comparability):

- Europe IT services (broad): USD 492B (2026E) ≈ €452B, but TEBS-eligible is only the managed services/outsourcing/implementation subset (Mordor Intelligence).

- Europe managed services (subset proxy): USD 95.6B (2025E) ≈ €88B (ReportsnReports / Market Data Forecast).

- Europe TIC: USD 69.27B (2026E) ≈ €64B (Mordor Intelligence).

- Europe insurance brokerage (broad): USD 260.03B (2025E) ≈ €239B, but TEBS-eligible is the portion where brokerage is workflow-embedded (commercial/specialty admin, platforms, MGA-like distribution infrastructure), not the entire premium-linked distribution ecosystem (Mordor Intelligence).

(Sources: Mordor Intelligence sector reports; ReportsnReports; Market Data Forecast—see Sources section.)

2.1.2 Sub-Sector Scale, Growth, and “TEBS-Eligible” Decomposition (15 Sub-Sectors)

How to read Table 2.1.2:

- Gross Sector TAM (€B) reflects the broad market size typically quoted in industry reports.

- TEBS-Eligible TAM (€B) is the addressable revenue pool under this report’s definition (Chapter 1), i.e., where tech enablement is an investable lever and can credibly move the business along the services-to-software continuum.

- Fragmentation metrics are presented as indicative and Europe-wide, recognizing meaningful country-by-country variation.

Table 2.1.2 — European TEBS landscape snapshot (2025E unless noted)

| Sub-Sector | Gross Sector TAM (€B) | TEBS-Eligible TAM (€B) | Eligibility Factor (range) | Growth (CAGR %) | Fragmentation (qual.) | CR5 (indic.) | HHI band (indic.) | Tech Leverage | Labor Intensity | Typical EBITDA Margins | Indicative Multiple Range (EV/EBITDA) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 3.1 IT Managed Services & Outsourcing | 80–100 | 80–100 | ~100% | 5–10% | High (mid-market) | 5–15% | 100–500 | High | Medium | 12–20% | 8–14× |

| 3.2 Testing, Inspection & Certification (TIC) | 55–70 | 40–55 | 60–80% | 3–5% | Moderate | 30–45% | 1,200–2,200 | Medium-High | Medium | 12–18% | 10–16× |

| 3.3 Professional Staffing & Recruitment | 100–130 | 25–40 | 20–30% | 4–6% | Very High | 10–25% | 150–700 | Low–Medium | Very High | 3–8% | 6–10× |

| 3.4 Compliance, Regulatory & Advisory | 20–30 | 15–25 | 70–85% | 6–9% | High | 10–20% | 200–900 | Medium-High | Medium | 15–25% | 8–14× |

| 3.5 Healthcare Services (Clinical/Dental/Vet) | 40–55 | 20–30 | 45–60% | 5–8% | Very High | 5–10% | 50–400 | Medium | High | 15–25% | 10–16× |

| 3.6 Financial Back-Office & Fund Administration | 25–35 | 20–30 | 75–90% | 5–8% | Moderate-High | 30–45% | 900–1,800 | High | Medium | 18–30% | 10–15× |

| 3.7 Engineering & Technical Consulting | 45–60 | 15–25 | 30–40% | 3–5% | High | 15–25% | 250–900 | Medium | High | 8–15% | 7–11× |

| 3.8 Facilities Management & Building Services | 70–90 | 15–25 | 15–30% | 3–5% | Very High | 20–30% | 300–1,200 | Low–Medium | Very High | 5–12% | 6–9× |

| 3.9 Marketing Services & Digital Agencies | 30–40 | 12–20 | 40–50% | 4–7% | Very High | 5–10% | 50–400 | Medium | High | 10–18% | 5–10× |

| 3.10 Education & Training Services | 15–25 | 7–12 | 40–55% | 5–8% | High | 5–15% | 80–600 | Medium-High | Medium-High | 10–20% | 7–12× |

| 3.11 Environmental & Sustainability Consulting | 10–18 | 6–12 | 60–75% | 8–12% | Very High | 5–10% | 50–400 | Medium | Medium-High | 12–20% | 8–13× |

| 3.12 Legal Services & LPO | 20–30 | 8–15 | 35–55% | 3–5% | High | 5–10% | 50–500 | Low–Medium | Very High | 15–30% | 7–12× |

| 3.13 Data & Analytics Services | 15–25 | 15–25 | ~100% | 8–12% | High | 15–30% | 400–1,400 | Very High | Medium | 15–25% | 10–16× |

| 3.14 Logistics & Supply Chain Services (asset-light/tech-enabled) | 50–70 | 15–25 | 25–40% | 4–6% | High | 20–35% | 500–1,600 | Medium-High | High | 5–12% | 7–11× |

| 3.15 Insurance Brokerage & Distribution | 40–60 | 25–40 | 55–70% | 6–8% | High (below top tier) | 15–30% | 400–1,600 | High | Low–Medium | 20–35% | 10–16× |

Notes on the quantitative fragmentation metrics (CR5 / HHI):

- CR5 = estimated market share of the 5 largest providers in the relevant European sub-market (country-weighted where possible).

- HHI bands are indicative and used to enforce internal consistency (not to claim regulator-grade precision).

- These metrics vary materially by country and by segment definition (e.g., “TIC overall” vs “food testing labs”; “insurance brokerage overall” vs “SME commercial brokers”). This report uses them as screening scaffolding, not as definitive concentration statistics.

Key observations (now consistent with the sizing math):

- The gross services universe is enormous (~€600–800B across these categories), but the TEBS-eligible slice is narrower (~€350–450B). The investable TEBS perimeter is large enough to support many platforms, but small enough that definition discipline matters.

- Fragmentation is widespread; consolidation is uneven. TIC and fund administration show structurally higher concentration, while healthcare groups, marketing agencies, and many compliance/advisory niches remain long-tail.

- Multiples are driven more by revenue quality and workflow embedding than by sector labels. “IT services” is not automatically premium; “staffing” is not automatically low—sub-segment positioning determines both margin potential and exitability.

2.1.3 Fragmentation: Making the Buy-and-Build Premise Measurable (CR5/HHI)

Fragmentation is the underwriting prerequisite for buy-and-build. In this report it is assessed using two complementary lenses:

- CR5 (top-5 share): practical and intuitive for investors; supports quadrant placement.

- HHI (Herfindahl-Hirschman Index): captures “shape” of the market beyond just the top five, helpful where one player dominates a local market but the rest is long-tail.

Interpretation thresholds used consistently in this chapter and the matrix (Figure 2.4):

- High fragmentation: CR5 < 20% (typically HHI < ~800)

- Moderate fragmentation: CR5 ~ 20–35% (HHI ~800–1,800)

- Lower fragmentation / more consolidated: CR5 > 35% (HHI > ~1,800)

These thresholds are consistent with the qualitative fragmentation ratings shown in Table 2.1.2 and eliminate the prior draft’s quadrant-placement inconsistencies.

2.1.4 Labor Intensity vs. Scalability: The Trade-Off Investors Actually Underwrite

Labor intensity is not “bad”; it simply dictates where value creation must come from:

- High labor intensity tends to cap margin expansion from tech alone (because delivery still requires people), but can support strong buy-and-build returns if integration is straightforward and scale benefits are real (procurement, scheduling density, shared services).

- Lower labor intensity / higher tech leverage supports non-linear scaling (revenue growing faster than headcount), which is disproportionately rewarded at exit.

To make this measurable during screening, we use revenue per FTE (and, where available, EBITDA per FTE) as simple, comparable proxies.

Table 2.1.4 — Indicative revenue/FTE benchmarks (Europe mid-market; screening ranges)

| Sub-Sector | Revenue / FTE (indic.) | What “good” looks like in diligence |

|---|---|---|

| IT Managed Services | €140k–€220k | PSA discipline; automation; NOC leverage; >70% recurring |

| TIC | €120k–€200k | Route density; lab utilization; digital QA; cross-selling of certification bundles |

| Staffing | €250k–€450k (high pass-through) | Judge on GP/FTE and EBITDA/FTE, not revenue; low working-cap volatility |

| Compliance/Reg Advisory | €120k–€200k | Productized offerings; template/workflow reuse; subscription compliance monitoring |

| Healthcare groups (dental/vet) | €90k–€160k | Chair/clinician utilization; standardized procurement; centralized billing |

| Fund admin / back-office | €150k–€260k | High automation; low error rates; standardized onboarding; embedded portals |

| Engineering consulting | €110k–€180k | Reduced bench volatility; tooling reuse; IP-bearing delivery accelerators |

| Facilities management | €80k–€140k | Route density, scheduling, CAFM adoption; procurement scale; reduced subcontract leakage |

| Marketing agencies | €110k–€190k | Retainers; analytics-driven delivery; reusable creative systems; margin by service line |

| Education/training | €90k–€160k | Blended learning; content reuse; cohort scaling; enterprise contracts |

| Environmental/sustainability | €110k–€190k | Recurring reporting; software-assisted measurement; standardized audits |

| Legal/LPO | €90k–€160k | Workflow tooling; matter lifecycle management; offshore/onshore leverage; specialization |

| Data & analytics | €150k–€280k | Reusable data models; platform accelerators; high NRR |

| Logistics (asset-light) | €120k–€220k | Control-tower tooling; high shipment/FTE; low exception rates |

| Insurance brokerage | €180k–€320k | Admin platform leverage; low servicing cost; cross-sell penetration |

Important: these are screening heuristics, not universal truths. Staffing, for example, often looks “productive” on revenue/FTE due to pass-through revenue; investors should underwrite to gross profit per FTE and conversion, not headline revenue.

2.2 Why TEBS Is the Dominant European Mid-Market PE Theme

2.2.1 Europe-Specific Structural Drivers

Four structural features of the European economy make TEBS uniquely attractive for buy-and-build strategies:

1) Extreme SME density creates a deep long tail of acquisition candidates.

SMEs are central to the EU economy, accounting for a majority share of employment and a large share of value creation. SME density and the prevalence of founder-owned firms create unusually deep bolt-on pipelines across most business service categories (EPP Group; Statista; IfM Bonn—see Sources). This is particularly visible in sub-sectors where local relationships and language remain central (IT MSPs, brokers, compliance/advisory, many healthcare services).

2) Service-heavy GDP composition sustains secular outsourcing and specialization.

Services represent a large share of European GDP (TheGlobalEconomy.com—see Sources). Even where outsourcing penetration varies by region (e.g., DACH vs Nordics vs UK&I), cost inflation, security/compliance requirements, and skills scarcity continue to push SMEs toward external providers in IT operations, compliance, and specialist advisory.

3) Cross-border fragmentation amplifies bolt-on density (and protects defensibility).

Europe’s fragmentation is structural: language, procurement norms, regulation, and local go-to-market models keep markets regionally segmented. That increases the number of viable bolt-ons and allows platforms to build defensible regional scale (e.g., Benelux + DACH MSP, pan-Nordic compliance platform) rather than competing head-on with global incumbents.

4) Generational transition expands supply of motivated sellers.

Across multiple European countries, the aging of founders and limited succession options continue to support deal flow in sub-€50M EV services businesses—often independent of the macro cycle.

2.2.2 Why Buy-and-Build Often Outperforms Greenfield SaaS in European TEBS

Investment committees frequently ask why not deploy the same capital into pure software. The answer is not ideological—it is risk-adjusted value creation math:

- Entry multiples and underwriting visibility differ. Mid-market services platforms can often be entered at materially lower multiples than software, with immediate EBITDA and contracted cash flows (DealSuite European Monitor; CLFI—see Sources).

- Bolt-on density is unusually high in Europe. Add-ons are abundant and frequently founder-led; many can be acquired below platform multiples, creating a repeatable multiple-arbitrage engine (Bain buy-and-build research; Gain.pro—see Sources).

- Tech can be layered onto an existing revenue base. In TEBS, technology is often best deployed as a delivery and retention lever inside an operating platform—rather than as a standalone product searching for distribution.

2.2.3 Transferable Patterns from US Services Roll-Ups—and What’s Structurally Different in Europe

US roll-ups provide useful patterns:

- Multiple arbitrage remains foundational in buy-and-build (Bain).

- Continuous acquirers outperform through faster growth and margin expansion, driven by repeated M&A muscle memory and integration cadence (Bain; INSEAD Knowledge).

- Integration discipline (finance/control integration early; operating model clarity) separates winners from “collections of businesses” (Bain; INSEAD).

What is structurally different in Europe (and why it matters to TEBS):

- Regulatory perimeter is broader and less uniform cross-border. Insurance distribution, healthcare delivery, and certain compliance/TIC activities face licensing, professional standards, and conduct regimes that vary by country. This raises integration complexity (entity structuring, compliance oversight, supervision models) but can also increase defensibility for scaled platforms with strong governance.

- Labor regimes and worker representation can materially affect synergy timing (works councils, transfer of undertakings, local employment protections). Operational integration playbooks need localization.

- Data and privacy constraints (GDPR) are more central to cross-border platform design—especially in healthcare, insurance, and data/analytics—affecting how “one platform” is executed in practice.

- Public procurement exposure is higher in parts of facilities, training, and environmental services, shaping contract structure, inflation pass-through, and churn dynamics.

Net: the US playbook transfers, but Europe requires more deliberate governance, compliance architecture, and country-specific integration sequencing—especially in regulated sub-sectors.

2.3 The Services-to-Software Continuum

2.3.1 Mapping All 15 Sub-Sectors

The services-to-software continuum (Chapter 1, Section 1.2.2) scores each sub-sector on recurring revenue, workflow/software penetration, data leverage, labor intensity, and switching costs.

2.3.2 Where Value Accrues on the Continuum

Value accretion is not linear. The most material valuation step-ups tend to occur when a provider crosses two practical thresholds:

Transition 1: “Hours” → “Managed outcome” (~2.0 to ~3.0)

Standardized delivery, tool-assisted workflows, and measurable outcomes improve margin and underwriting confidence.

Transition 2: “Managed outcome” → “Embedded workflow” (~3.0 to ~4.0)

Client switching costs become operational (integrations, data models, portals, compliance routines), not just contractual.

2.3.3 Within-Sector Variance (Where Alpha Actually Comes From)

Within-sector variance often exceeds between-sector variance. An MSP with automated remediation, a standardized PSA stack, and >80% recurring behaves economically differently from a break-fix reseller—even though both are “IT services.” The sub-sector modules (Chapters 3–5) therefore emphasize target-level diagnostics over sector labels.

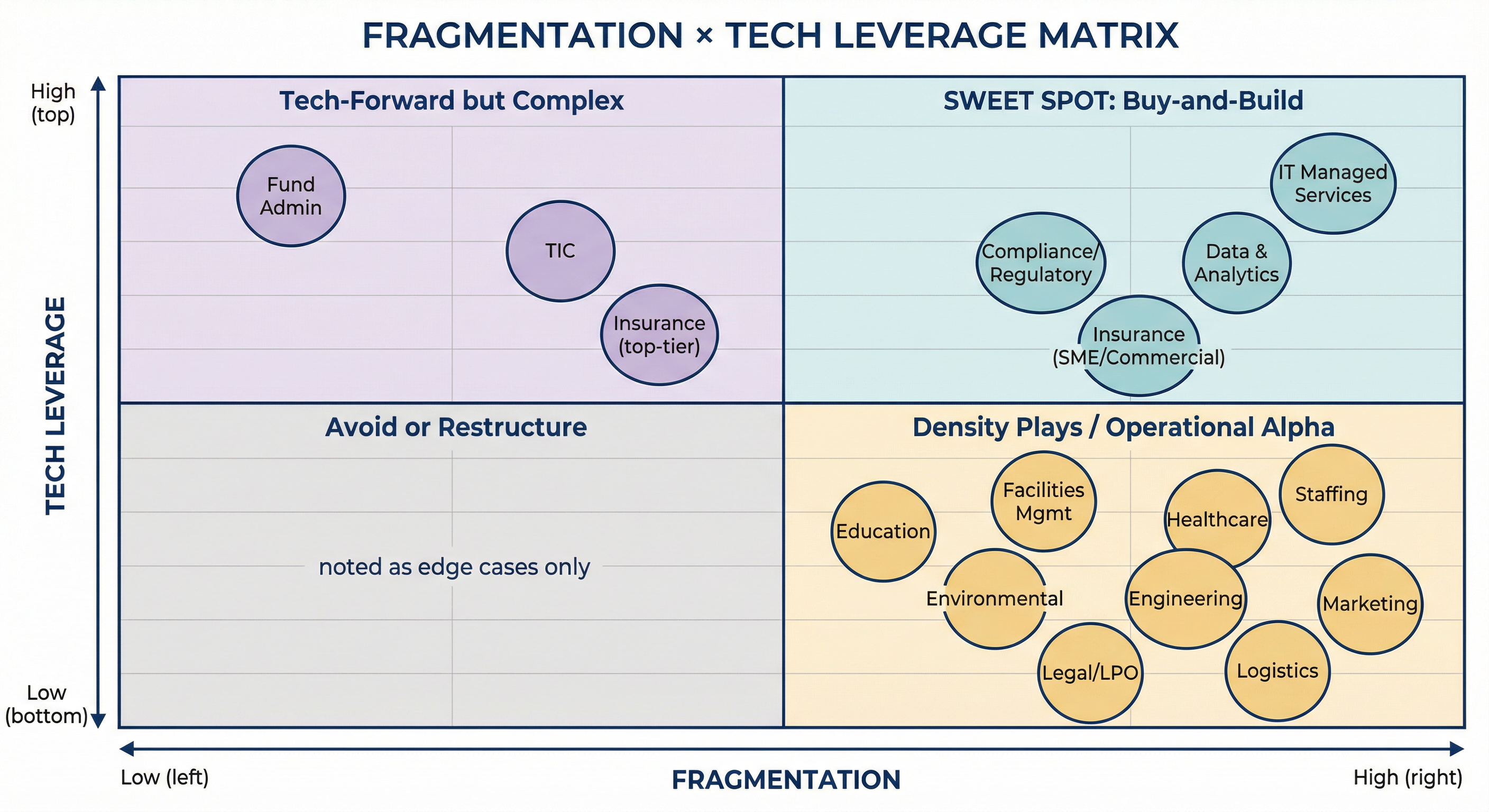

2.4 Fragmentation vs Tech Leverage Matrix

Critical fix implemented: The prior draft’s matrix was internally inconsistent with Table 2.1.2 fragmentation ratings. This refined matrix:

- Uses x-axis = fragmentation (low → high), consistent with the buy-and-build intuition that “more fragmented” sits to the right.

- Places each sub-sector in a quadrant consistent with Table 2.1.2 and the CR5/HHI bands.

- Includes TIC (3.2), which was previously missing.

Quadrant I — “Sweet Spot Buy-and-Build” (high fragmentation + high tech leverage):

IT MSPs, compliance/regulatory services, data & analytics, and many workflow-embedded insurance brokerage segments combine: (i) repeatable service delivery, (ii) meaningful tech leverage, and (iii) dense bolt-on pipelines.

Playbook: platform + rapid bolt-ons; centralize data/tech stack; standardize go-to-market and reporting.

Quadrant II — “Tech-forward but more consolidated / integration-heavy”:

Fund administration and portions of TIC exhibit higher concentration and more complex integration constraints (systems, accreditation, regulated processes).

Playbook: fewer, higher-quality deals; heavier diligence on systems and governance; prioritize integration architecture early.

Quadrant IV — “Density plays / operational alpha”:

Staffing, facilities, healthcare group roll-ups, and several advisory categories can be excellent buy-and-build arenas, but the tech premium requires deliberate repositioning (workflow, scheduling, billing, analytics) rather than assuming it.

Playbook: scale + shared services + procurement + scheduling density; selective tech overlay tied to measurable unit economics.

2.5 Valuation Drivers Framework: What Separates 6× from 12× EBITDA

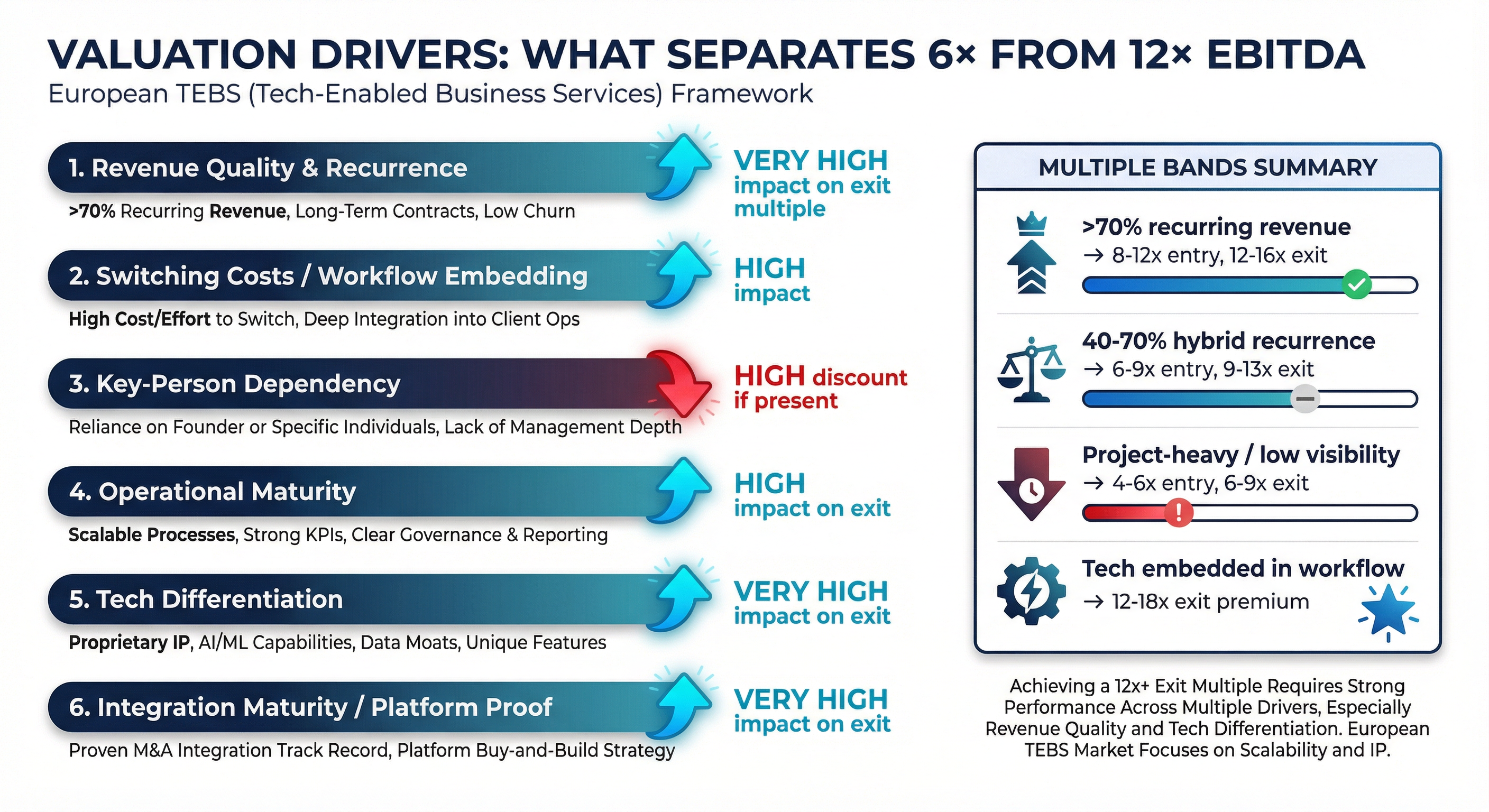

2.5.1 The Six-Driver Framework

Building on Chapter 1 (Section 1.6.2), valuation outcomes in TEBS are best explained by six drivers that map to both entry pricing and exit narrative strength. Sector-level multiple ranges exist, but quality dispersion within the same sub-sector is often larger than inter-sector dispersion (DealSuite; CLFI—see Sources).

| Driver | Impact on Entry Multiple | Impact on Exit Multiple | Key Diligence Signal |

|---|---|---|---|

| 1. Revenue Quality & Recurrence | High | Very High | % under contract; renewal mechanics; NRR where measurable |

| 2. Switching Costs / Workflow Embedding | Medium | High | Integrations, portals, data models; operational reliance |

| 3. Key-Person Dependency | High discount if present | Must be solved | Producer concentration; bench depth; account governance |

| 4. Operational Maturity | Medium | High | KPI cadence; cohort margins; unit economics; forecasting accuracy |

| 5. Tech Differentiation | Medium-High | Very High | Proprietary workflow; automation; client-facing tooling vs back-office-only |

| 6. Integration Maturity / Platform Proof | N/A at entry | Very High | Standardized systems; synergy capture; repeatable M&A engine |

2.5.2 The Driver-to-Multiple Linkage Table

| Observable Condition | Typical Multiple Band (Mid-Market Entry) | Typical Multiple Band (Platform Exit) | What Makes the Difference |

|---|---|---|---|

| Recurring/contracted revenue >70% | 8–12× | 12–16× | Underwriteable cash flows; lower perceived cyclicality |

| Hybrid recurrence (40–70%) | 6–9× | 9–13× | Exit depends on proving recurrence conversion and retention |

| Project-heavy / low visibility | 4–6× | 6–9× | Needs explicit conversion story (contracts, productization) |

| Top 10 clients <30% | +0.5–1.0× vs peer | Sustains premium | Diversification reduces “event risk” |

| Top 3 clients >40% | -1–2× vs peer | Exit constrained | Concentration is a recurring value killer in services |

| Tech embedded in client workflow | 8–12× | 12–18× | Switching costs are operational, not just relational |

| Federated group, weak integration | N/A | Discount at exit | “Collection of assets” narrative limits multiple expansion |

2.5.3 PE vs Corporate Buyers (and Why It Matters in TEBS)

Observed market data indicates that buyer type influences multiples, with PE often paying more when a credible value-creation pathway exists, while corporates may price more tightly unless synergies are immediate (CLFI—see Sources). In TEBS, this dynamic is strongest where secondary buyout exit paths are deep (e.g., IT services, insurance distribution infrastructure, healthcare group platforms) and weakest in commoditized, low-differentiation segments.

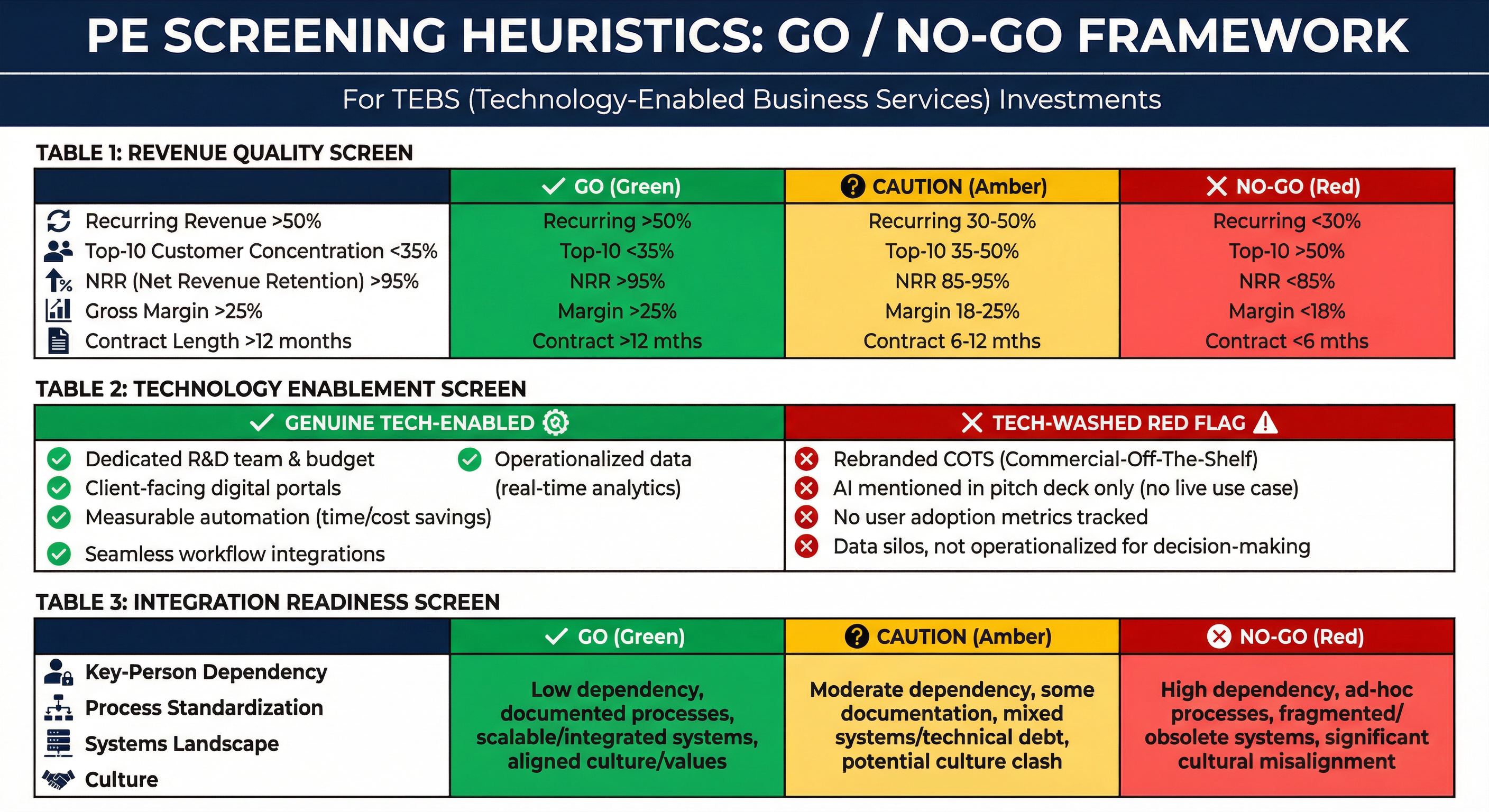

2.6 PE Screening Heuristics: Go/No-Go Decision Framework

These heuristics translate the valuation drivers into actionable screening filters.

2.6.1 Revenue Quality Screen

| Criterion | Go | Caution | No-Go |

|---|---|---|---|

| Recurring/contracted revenue share | >50% | 30–50% | <30% with no credible conversion plan |

| Top 10 concentration | <35% | 35–50% | >50% (or single client >20%) |

| Net revenue retention (where measurable) | >95% | 85–95% | <85% structural churn |

| Gross margin (service context) | >25% | 18–25% | <18% commodity profile |

| Contract duration | >12 months | 6–12 months | <6 months / transactional |

2.6.2 Technology Enablement Screen

| Criterion | Genuine Tech-Enabled | “Tech-Washed” (Red Flag) |

|---|---|---|

| R&D / product capability | Dedicated team; sustained spend | Rebranded COTS tools; no product ownership |

| Client-facing tech | Portals/dashboards that change switching costs | “AI” in deck; no demo; no adoption metrics |

| Delivery automation | Measurable reduction in labor per unit | Manual delivery; automation claims not reflected in unit economics |

| Data leverage | Data improves delivery outcomes and retention | Data collected but not operationalized |

| Workflow embedding | Integrations + process reliance | Client can switch with minimal migration |

2.6.3 Integration Readiness Screen

| Criterion | Go | Caution | No-Go |

|---|---|---|---|

| Key-person dependency | Distributed revenue ownership | 2–3 key individuals | Founder controls >30% of revenue + all relationships |

| Process standardization | SOPs + KPI cadence | Partial documentation | No unit economics; bespoke everything |

| Systems landscape | Modern PSA/ERP/CRM + APIs | Mixed legacy | Undocumented legacy core; no migration path |

| Culture | Professional management | Founder-led but open | Resistant, litigious, high attrition |

2.6.4 Fake Tech-Enablement Detection Checklist

Common “tech premium traps”:

- AI claims without demonstrable client product adoption.

- “Platform” that is effectively a file-sharing portal.

- No improvement in productivity metrics (e.g., stable/declining gross profit per delivery FTE).

- “Recurring” revenue that is relational rather than contractual.

- “Tech spend” that is IT maintenance rather than product capability.

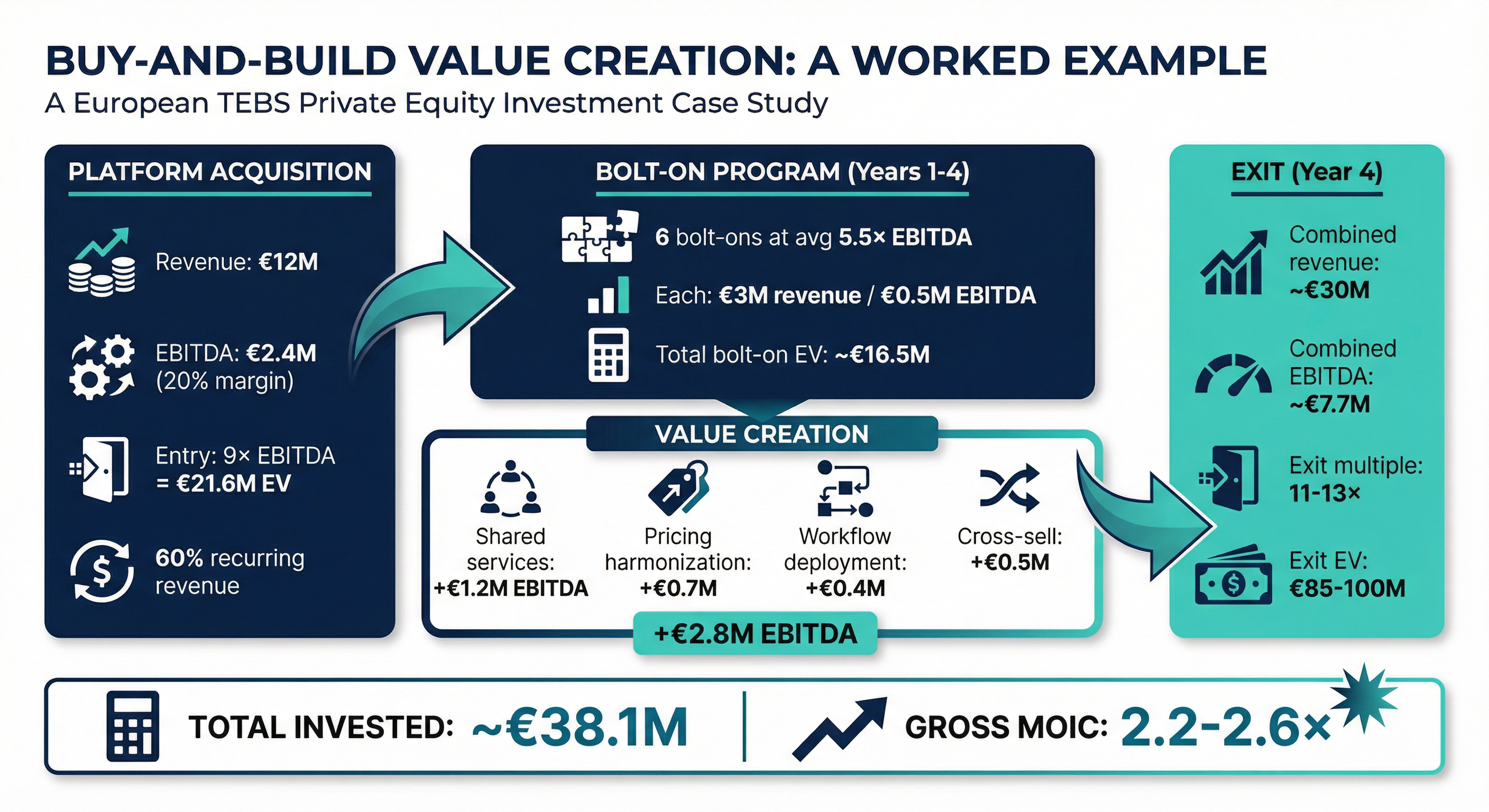

2.7 The Economics of Buy-and-Build in European TEBS: A Worked Example

A stylized but representative mid-market thesis:

Platform acquisition: Compliance advisory firm; €12M revenue, €2.4M EBITDA (20%); entry at 9× EBITDA (= €21.6M EV); 60% recurring; workflow tool used in delivery.

Bolt-on program (years 1–4): Six bolt-ons at average 5.5× EBITDA; each €3M revenue / €0.5M EBITDA; total bolt-on EV ≈ €16.5M.

Value creation levers (illustrative):

- Shared services centralization: +€1.2M EBITDA

- Pricing harmonization: +€0.7M EBITDA

- Platform workflow deployment: +€0.4M EBITDA

- Cross-sell incremental revenue (€2M at 25% margin): +€0.5M EBITDA

Exit (year 4):

- Combined revenue: ~€30M

- Combined EBITDA: ~€7.7M

- Exit multiple: 11–13× (credible workflow/recurrence/platform proof)

- Exit EV: ~€85–100M

Total invested EV: ~€38.1M

Gross MOIC: ~2.2–2.6× (pre-leverage)

This example illustrates the core TEBS return engine: multiple arbitrage + integration synergies + tech-enabled operational leverage, with the exit multiple earned through platform proof rather than assumed at entry.

2.8 Implications for Portfolio Construction and Chapter Sequencing (Completed Table)

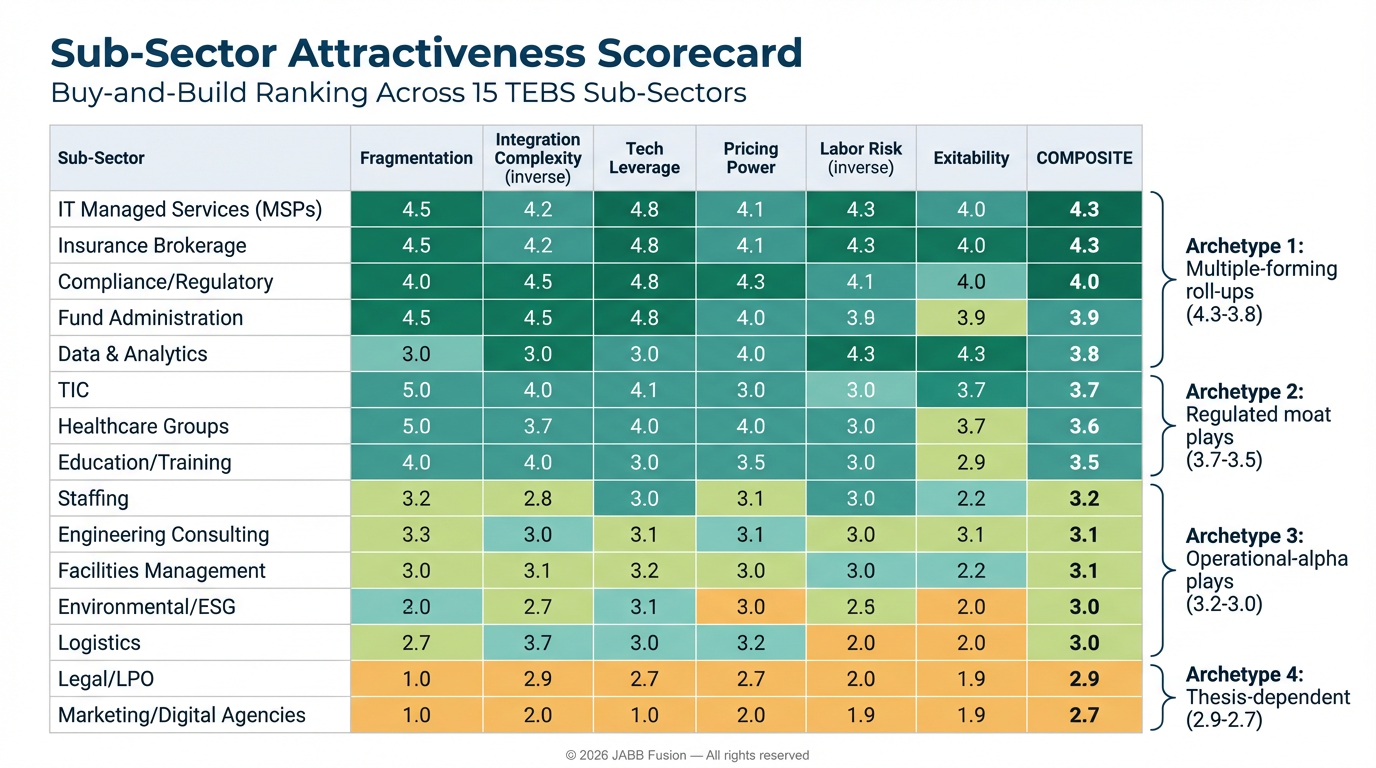

This chapter’s sizing, fragmentation metrics, and frameworks translate into practical portfolio construction:

- Prioritize Quadrant I for platform theses where tech leverage and fragmentation jointly support both bolt-on density and multiple expansion.

- Use Quadrant II selectively where consolidation is more advanced; returns depend on operational excellence and governance-heavy integration.

- Treat Quadrant IV as an operational-alpha arena: scale economics are real, but the tech multiple must be built, not expected.

- Avoid “Quadrant III-style” traps (low tech leverage + high integration complexity) unless there is a clear productization plan.

Table 2.8 — Portfolio construction implications by quadrant (full)

| Quadrant | Priority Sub-Sectors (from Fig. 2.4) | Core Value Lever | Integration Reality | Typical Exit Narrative | Typical Exit Multiple Band* |

|---|---|---|---|---|---|

| I — Sweet Spot (High frag / High tech) | IT MSP (3.1); Compliance (3.4); Data & Analytics (3.13); Insurance brokerage segments (3.15) | Multiple arbitrage + tech standardization + cross-sell | Moderate; manageable if systems/process discipline exists | “Workflow-embedded platform with recurring revenue and proven bolt-on engine” | ~10–16× |

| II — Tech-forward but more consolidated | Fund admin (3.6); TIC (3.2); parts of insurance top-tier (3.15) | Operational excellence + governance + selective M&A | Higher; systems/accreditation/regulatory complexity | “Scaled specialist with strong controls, compliance moat, and platform-grade reporting” | ~10–16× |

| IV — Density plays / ops alpha (High frag / Lower tech) | Staffing (3.3); Facilities (3.8); Healthcare groups (3.5); Education (3.10); Environmental (3.11); Engineering (3.7); Marketing (3.9); Legal/LPO (3.12) | Density, shared services, procurement, scheduling; then selective tech overlay | Often lower per-deal, but needs strong operating model | “Scaled regional consolidator with standardized operations and improving unit economics” | ~6–12× |

| III — Consolidated & low tech (generally avoid) | (Few core TEBS targets by definition; appears in edge cases) | Turnaround only | Often unattractive risk-return | “Restructuring story” | Case-specific |

*Bands are indicative and depend heavily on revenue quality, recurrence, and platform proof (Section 2.5).

How this drives chapter sequencing (Chapters 3–5):

- We lead with sub-sectors that repeatedly screen well under the combined lenses of fragmentation + tech leverage + integration feasibility (especially IT MSPs, compliance-led services, TIC segments with roll-up opportunity, and workflow-embedded insurance distribution infrastructure).

- Quadrant IV sectors follow with a different underwriting stance: operational playbook first, tech second, with explicit labor intensity diagnostics.

Chapter 3: Sub-Sector Deep Dives (Modules 3.1–3.5): Platform Fundamentals in High-Activity TEBS Arenas

This chapter delivers the first five standalone sub-sector modules, each following the identical A–H structure defined in Chapter 1 (Section 1.6.1). The five sub-sectors—IT Managed Services & Outsourcing, Testing Inspection & Certification (TIC), Professional Staffing & Recruitment, Compliance Regulatory & Advisory Services, and Healthcare Services—are among the most actively traded arenas in European mid-market PE and illustrate the core economic tension of TEBS buy-and-build: whether consolidation creates a technology-powered platform (repeatable processes, workflow embedding, scalable margins) or merely a scaled services group (headcount aggregation with limited multiple resilience).

Consistency note (TAM + rubric):

- Market sizing below is consistent with the gross TAM vs TEBS-eligible TAM construct in Chapter 2 (Table 2.1.2). Where published market estimates diverge meaningfully, we name the sources, explain the definitional gap, and then state the report’s TEBS-eligible working range.

- Scoring aligns to the six-dimension rubric in Chapter 1 (Section 1.6.2): Fragmentation, Integration Complexity (inverse-scored), Tech Leverage, Pricing Power, Labor Risk (inverse-scored), Exitability. “Bolt-on density” and “standardization potential” are treated as supporting evidence within these six dimensions (not additional dimensions), resolving the prior inconsistency.

Each module includes: (i) a mandatory diligence-ready table with source-footnoted benchmarks where available; (ii) a Platform Design Snapshot; and (iii) IC-ready insights. Each module also includes a short AI impact teaser bridging to Part V and a more granular labor lens bridging to Part VI.

3.1 IT Managed Services & Outsourcing (MSPs/MSO)

A. Definition & Scope

IT Managed Services & Outsourcing (MSP/MSO) covers outsourced management of an organization’s IT infrastructure, end-user environments, cloud platforms, and security operations under recurring contracts. In scope: managed infrastructure, managed security (SOC/MDR), managed cloud (admin + FinOps), managed networks/communications (SD-WAN/UCaaS ops), and co-managed IT. Out of scope: pure project-based IT consulting, bespoke software development, and hardware resale without a contracted service wrapper.

Where “tech-enabled” shows up in practice: Delivery depends on PSA/RMM, ticketing/ITSM, endpoint tooling, and increasingly automation. Switching costs are created by embedded tooling, documentation, identity/device posture, and operational routines—not just contractual term.

B. Market Size, Growth, and Fragmentation (with explicit reconciliation)

Chapter 2 cross-reference: Ch2 Table 2.1.2 frames MSP/MSO at ~€80–100B TEBS-eligible TAM (subset of a broader “managed services / IT outsourcing” spend pool).

Why published estimates vary (and how we reconcile them):

- Some sources define “managed services” narrowly (recurring managed IT), while others include broader IT outsourcing categories (e.g., large-scale enterprise ITO, certain hosting, systems integration wrappers). This creates large range dispersion (e.g., one 2025 estimate around ~$59B vs another around ~$95B for “Europe managed services,” each with different inclusions).

- For this report, TEBS-eligible MSP/MSO excludes (i) pure hardware resale, (ii) predominantly project consulting, and (iii) portions of enterprise ITO where value creation is dominated by labor-arbitrage megadeals rather than mid-market platform economics. The working range remains €80–100B, consistent with Ch2, and is best interpreted as “investable, recurring, mid-market-weighted managed services” rather than total European IT outsourcing.

Sources: definitional dispersion evidenced across market reports (e.g., Mordor Intelligence vs other syndicated research aggregators).

Fragmentation: The mid-market is highly fragmented across most European countries: thousands of sub-€15M revenue MSPs, typically founder-led, with local density driven by proximity/language preferences and on-site requirements for parts of delivery. Concentration is meaningfully higher at the global/enterprise end; it is structurally lower in SME-serving MSPs.

Directional concentration note (no unsupported CR5 claims): Reliable, comparable CR5 figures for “SME MSPs” are rarely published due to classification noise. In diligence, sponsors should compute concentration country-by-country using Orbis/Companies House/Amadeus lists filtered by revenue band and NACE codes, then adjust manually for “true MSP vs reseller vs project IT” revenue mix (Chapter 8 toolkit).

C. Typical Target Profile

| Attribute | Typical Range |

|---|---|

| Revenue | €3–30M |

| EBITDA margin | 12–20% (security-led often higher; break-fix heavy often lower) |

| Ownership | Founder-led (common) or first-gen PE-backed platforms |

| Geography | Single-country; often single-region with adjacency expansion potential |

| Recurring revenue | 65–85% (contracted recurring) |

| Employees | 30–250 FTE |

| Client base | 50–500 SME/mid-market clients; top-10 often <30% revenue |

D. Buy-and-Build Attractiveness (six-dimension rubric)

- Fragmentation: 5/5. Large long tail of founder-led assets; succession-driven supply remains strong.

- Integration complexity (inverse-scored): 4/5. Integration is operationally repeatable when a clear tool-stack migration plan exists; primary friction is tool sprawl + service-catalog inconsistency.

- Tech leverage: 4.5/5. Material value can be created via automation, standardization, monitoring, and security tooling embedded into client workflows.

- Pricing power: 4/5. Switching costs + criticality support price realization, especially when tied to security/compliance outcomes.

- Labor risk (inverse-scored): 3/5. Persistent shortage risk for cloud/security engineers; mitigants include nearshoring, automation, and tiered delivery models. External labor indicators (Eurostat vacancy rates; cybersecurity workforce studies) should be used as macro context, but underwriting should be based on actual time-to-hire, wage inflation, and attrition in the platform footprint.

- Exitability: 4.5/5. Deep sponsor-to-sponsor bid stack; strategics also active for scaled assets.

Composite (indicative): 4.3/5.

E. Technology Levers (incl. AI teaser)

Core systems: PSA (e.g., ConnectWise, Autotask), RMM (e.g., NinjaOne, Datto, N-able), ITSM/ticketing, identity/device management, EDR/MDR, SIEM/SOC platforms, documentation/knowledge base.

Automation & AI (value + risk teaser for Part V):

- Opportunity: AI-assisted triage, summarization, and guided remediation can reduce L1/L2 effort, increase first-contact resolution, and improve SLA compliance. Over 12–24 months, AI copilots can shift the labor mix toward fewer L1 tickets per endpoint and higher engineer leverage.

- Threat: If “good enough” AI-driven IT support becomes productized by software vendors/hyperscalers, parts of commodity support risk compression—pushing MSPs to differentiate with security outcomes, compliance, and verticalized offerings.

EBITDA impact (more precise timeline ranges):

- PSA/RMM standardization: typically +150–300 bps EBITDA within ~6–12 months post-migration via utilization discipline, ticket leakage reduction, and billing accuracy (benchmark ranges drawn from operator playbooks and MSP integration case studies; validate per-asset with pre/post KPI baselines).

- Procurement + vendor rationalization: often +100–200 bps within ~6–18 months (licenses, tools, connectivity).

- Automation (scripts + AI triage) + tiered delivery: typically +150–350 bps within ~12–24 months depending on starting maturity and ticket volume profile.

F. Value Creation Playbook (with quantified uplift expectations)

Months 0–12: Foundation (target: +200–400 bps EBITDA)

- Financial integration + unified KPI pack in 30–60 days

- PSA/RMM migration plan signed in first 60 days; execute within 6–9 months

- Centralize procurement + vendor standardization (licenses, security stack)

- Service catalog + SLA normalization; reprice out-of-market legacy contracts

- Establish shared-services NOC (Tier 1) and security baseline (MDR partner or internal SOC-lite)

- Commercial: convert break-fix tails into managed bundles; attach security add-ons

Months 12–36: Scale & Differentiate (target: additional +200–500 bps EBITDA)

- Expand centralized NOC/SOC, 24/7 where justified; introduce tiered support model

- Nearshore Tier 1/2 where culturally/linguistically feasible (CEE hubs) to offset wage pressure

- Verticalize (regulated SMB verticals: healthcare, financial services, industrial) with compliance-aligned bundles

- Productize reporting: client portal dashboards + QBR (quarterly business review) cadence

- Execute bolt-ons (geographic adjacency first; then capability add: security, cloud optimization/FinOps)

G. Buyer Landscape (corrections + sourcing discipline)

Sponsor and strategic interest remains high due to recurring revenue, mission-criticality, and scalable integration playbooks. Competitive processes are most intense for assets with: (i) high contracted recurring revenue; (ii) low concentration; (iii) tool-stack maturity; and (iv) credible security-led upsell.

Corrected deal/date: 3i’s investment in Constellation was announced in May 2024 (not January 2025).

Other buyer notes (avoid unsupported “% of assets PE-backed” claims): A meaningful and growing portion of European MSP platforms are sponsor-owned, but published “share of assets in PE portfolios” estimates are inconsistent and often methodology-dependent. This report treats sponsor saturation as qualitative and recommends tracking it empirically via (i) PE deal databases and (ii) country-level platform mapping during origination (Chapter 7 tools).

Exit dynamics: Secondary exits dominate; strategics (integrators/telecoms) are relevant for scaled, multi-country or security-differentiated platforms.

H. Red Flags & Failure Modes (incl. labor + AI)

- “Managed” revenue that is actually project/break-fix: If a large share is ad hoc, retention and margin stability are overstated.

- Tool-stack sprawl post-acquisition: Failure to standardize PSA/RMM within 6–9 months prevents shared-services leverage and makes KPI comparability impossible.

- Founder-led sales dependency: Underwrite a documented relationship transition plan; require account ownership transfer and multi-threading.

- Labor squeeze without delivery redesign: Wage inflation + scarcity in cloud/security can erase the integration thesis unless mitigated via nearshore, automation, and tiering.

- Paying “platform multiples” without platform attributes: Entry >~12× EBITDA requires defensible differentiation (security outcomes, verticalization, high NRR); otherwise multiple compression risk dominates.

Platform Design Snapshot — IT Managed Services